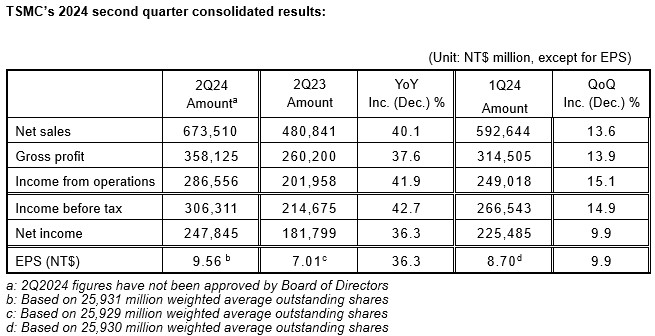

Q2 gross margin was 53.2%, operating margin was 42.5%, and net profit margin was 36.8%.<

In Q2 shipments of 3nm accounted for 15% of total wafer revenue; 5nm accounted for 35%; 7nm accounted for 17%. Advanced technologies, defined as 7nm and more advanced technologies, accounted for 67% of total wafer revenue.

“Our business in the second quarter was supported by strong demand for our industry-leading 3nm and 5nm technologies, partially offset by continued smartphone seasonality,” said CFO Wendell Huang,“moving into third quarter 2024, we expect our business to be supported by strong smartphone and AI-related demand for our leading-edge process technologies.”

The AI boom has propelled HPC to become TSMC’s biggest applications market taking 52% of total revenues, with smartphone second on 33% of revenues and Auto, IoT etc taking 15%.

2024 capex is expected to be between $30 billion and $32 billion.

Mass production on 2nm is scheduled for H2 2025 with an updated 2nm process in production in 2026 and a 1.6nm process in production in H2 2026.

CoWos packaging availability will be constrained through 2025 although capacity has doubled for last year and may double again next year, “From last year to this year, we have more than doubled and we may next year,” said CEO C.C.Wei.

On the use of the possible future packaging technology of side-by-side panel mounting, Wei said: “Three years later, I believe panel fan-out technology will start to be introduced, and we are working on it and we will be ready for it.”

Based on the Company’s current business outlook, management expects the overall performance for third quarter 2024 to be as follows:

Revenue is expected to be between $22.4 billion and $23.2 billion;

And, based on the exchange rate assumption of US$1 to NT$32.5:

Gross profit margin is expected to be between 53.5% and 55.5%;

Operating profit margin is expected to be between 42.5% and 44.5%.